Adjustments to the impak methodology

impak announces adjustments to its rating methodology, adopted in February 2023. The adjustments involve changes to the impak Scores for the entire impak universe.

The current improved impak methodology consists of the following three adjustments:

(i) The introduction of the impak Materiality Score (iMS), a more robust identification process of relevant negative impacts for each sector which quantitatively weighs financial and stakeholder materiality

(ii) The introduction of a qualitative criterion of positive impact materiality to retain material activities for which exact revenues are not reported

(iii) And the increase of the threshold for controversies to be considered material

The impak Materiality Score (iMS)

In order to identify the most important outcomes, impak created the impak materiality score (iMS) and a threshold to better distinguish material outcomes from those that are non-material (less significant). The integration of this score into our materiality assessment allows us to be even more precise in targeting the issues most relevant to a sector and to better inform clients on the most pressing risks a company faces. This is the result of a two-year-long effort to bring together academic research and synthesize our expertise in impact and financial risk assessment into one common, actionable metric that is unique on the market.

The iMS is an aggregate score based on the financial and stakeholder materiality of negative outcomes from each ICB sector.

Stakeholder materiality score: focuses on the external impacts generated by an organization’s activities, including impacts on society and the environment. It is based on i) sector expertise value from impak’s industy leads’ knowledge, ii) hundreds of external sources and databases such as the Science-Based Targets Network sector materiality tool, the European Union list of sectors that highly contribute to climate change, and Transparency International’s Bribe Payers’ Index, and iii) value drivers identified by the SASB Standards. While these value drivers are purely financial, some of them can constitute proxy measures to evaluate the risk of negative impacts for certain outcomes.

Financial materiality score: focuses on economic value-creation, external issues that internally impact a company’s financial performance and its ability to create economic value for investors and shareholders. The financial materiality metric draws from work developed by Consolandi, Eccles, and Gabbi (2020). These authors published several papers aiming to assess the exposure of different sectors to various ESG factors. Using the value drivers dataset produced by SASB, they have developed the financial relevance indicator (FRI) to evaluate the level of financial relevance of any given sustainability risk for any given sector.

The iMS ranges from 0 (less material) to 4 (extremely material). Therefore, an impact will be considered “material” and retained for analysis if i) the iMS exceeds 2 and ii) the stakeholder materiality score exceeds 2.

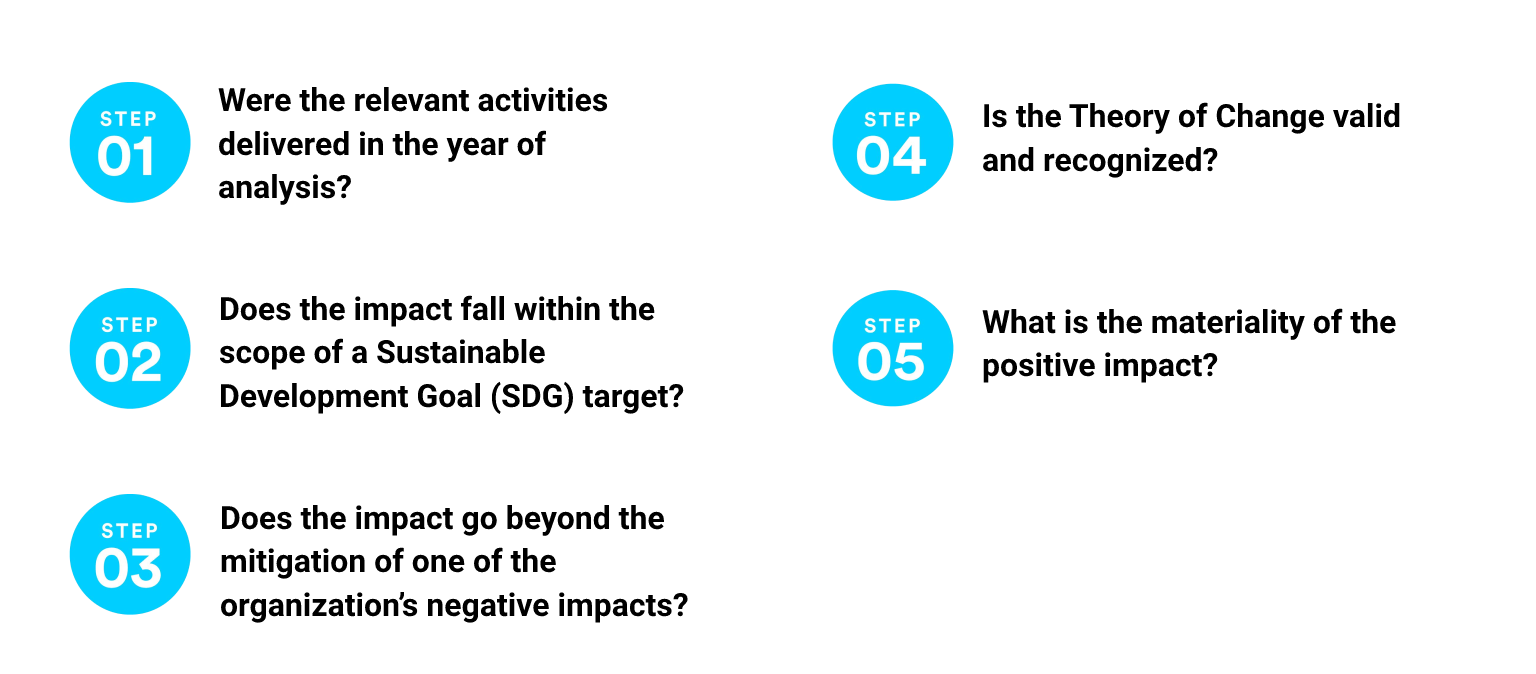

A qualitative assessment of positive impacts

The positive impact selection process comprises five steps (read the full infographic):

Given the frequent lack of financial data from corporations to assess positive activities based on the share of revenue (step 5), impak developed a new assessment method to retain positive impacts. In addition to our current quantitative assessment of financial materiality, it is now possible, as a second option, to assess the materiality of a positive activity through a qualitative assessment based on specific criteria.

For example, the criteria consider if the positive activity is part of the company’s core business, if the product or service represents one entire business line or if the company provides qualitative information to demonstrate that the product or service is substantial compared to its overall activities.

A threshold for controversies

Finally, based on empirical analysis, a new threshold was set for controversies to lead to an impact type “Z.” Until now, any material controversy (scoring above 3.25) could lead to a “Z” based on the scoring criteria.

As of February 2023, a new threshold was established: only controversies scoring above 4.5 (out of 10) will be eligible for a “Z.” Consequently, we only link High and Severe controversies to a “Z.”

You may also like

Annual impak Score review

Why single materiality is not good risk management