Is ESG becoming a four-letter word?… from ESG to ESGi

Is ESG becoming a four-letter word?… from ESG to ESGi

One of the hot topics this summer was what we like to call “The Big Great ESG Debate”. Something we, at impak, have been working on and writing about for years, but hey, we’re happy it finally caught the attention of mainstream media (despite not always being so happy as to how certain public leaders politicize the matter…). For those who haven’t followed, let us take a stab at summarizing things:

- Contrary to common thinking, ESG was never built to be a measure of sustainability, rather it is a measure of financial risk and materiality of E,S and G factors, i.e. the effect of ESG on a given company, often referred to as “outside-in” risks.

- Although the IFRS and its ISSB firmly defend this single materiality approach, Europe has taken another route and suggests referring to double materiality, which includes stakeholder materiality, i.e. adding the effects a company has on E, S and G or the “inside-out” dimension. Seems obvious doesn’t it ? By the way, back in 2020, we argued in our “impact alpha” paper that, on top of simply making sense from an ethical point of view and in the long-term, stakeholder materiality is also financially material.

- E, S and G are inextricably linked, and trying to focus on one letter rather than the full picture (as proposed by The Economist) is, to say the least… missing the full picture.

- The same goes for SDGs, which have now become a consensus for defining sustainability and positive impact.

In response to this, many of our peers have come out with “SDG scores” to complement their ESG ratings and offer investors data to back their sustainable investment claims, something we’ve been offering since 2019. This is great (honestly). And it finally gives us a chance to compare our ratings on an (almost) apples to apples basis.

This is what this paper is aimed at, after a quick methodological introduction, we compare our impak Scores against RobecoSAM’s SDG scores for a given sample of companies showcased in their recent paper*, as well as against the ESG ratings of 4 prominent ESG rating agencies (Sustainalytics, MSCI, S&P ESG & Refinitiv).

ESG vs impact 101

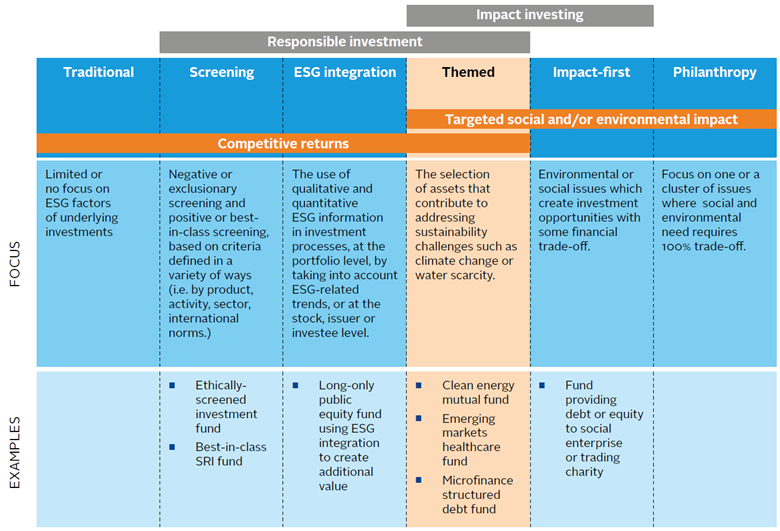

Sustainable financing / investing has become a very broad term that encompasses many things. We like to use the following to visualize the spectrum of options available to lenders / investors.

Figure 1: the sustainable investing spectrum

Now, a few consensual definitions around impact:

- An impact is a change in an outcome caused by an organization. An impact can be positive or negative, intended or unintended.

- An outcome is the level of well-being experienced by a group of people, or the condition of the natural environment, as a result of an event or action.

- The impact management is the process of identifying the positive and negative impacts that an enterprise has on people and the planet, and then reducing the negative and increasing the positive.

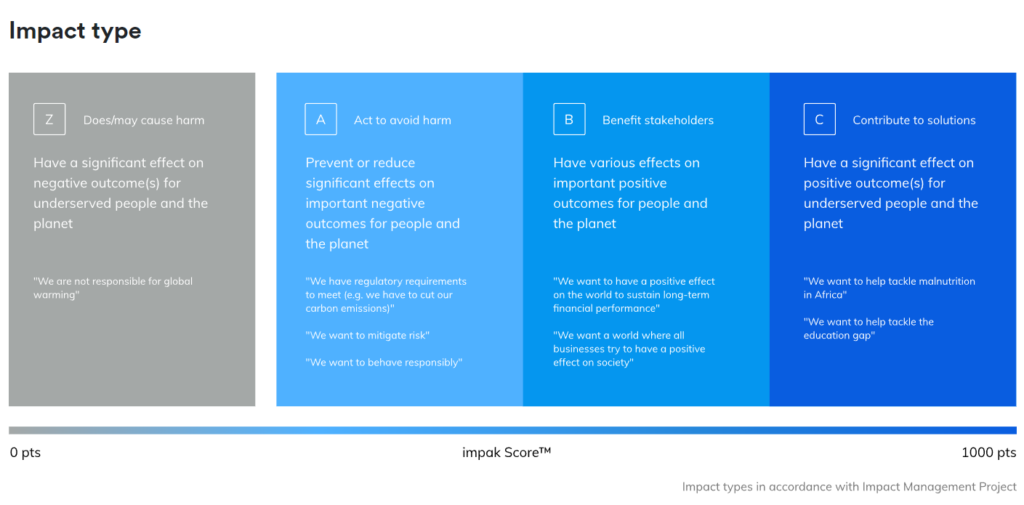

Another useful way to look at it is by using the ABCs of impact management developed by the Impact Management Project (now housed at Impact Frontiers), with which the impak methodology and impak score is aligned. So good ESG scoring companies would be in the A category, and low ESG scoring companies would be in the Z category. But ESG doesn’t capture the B’s and the C’s.

Figure 2: the ABCs of impact management

So where does all this bring us? The issue is that (i) some ratings claim to measure “impact” where they do not, at best they measure alignment with SDGs, sometimes based on dubious, opaque and undisclosed methodologies, and (ii) a lot of investors claim to be in the themed category while only using ESG ratings, which clearly places them in the ESG integration category.

From double materiality to… materiality

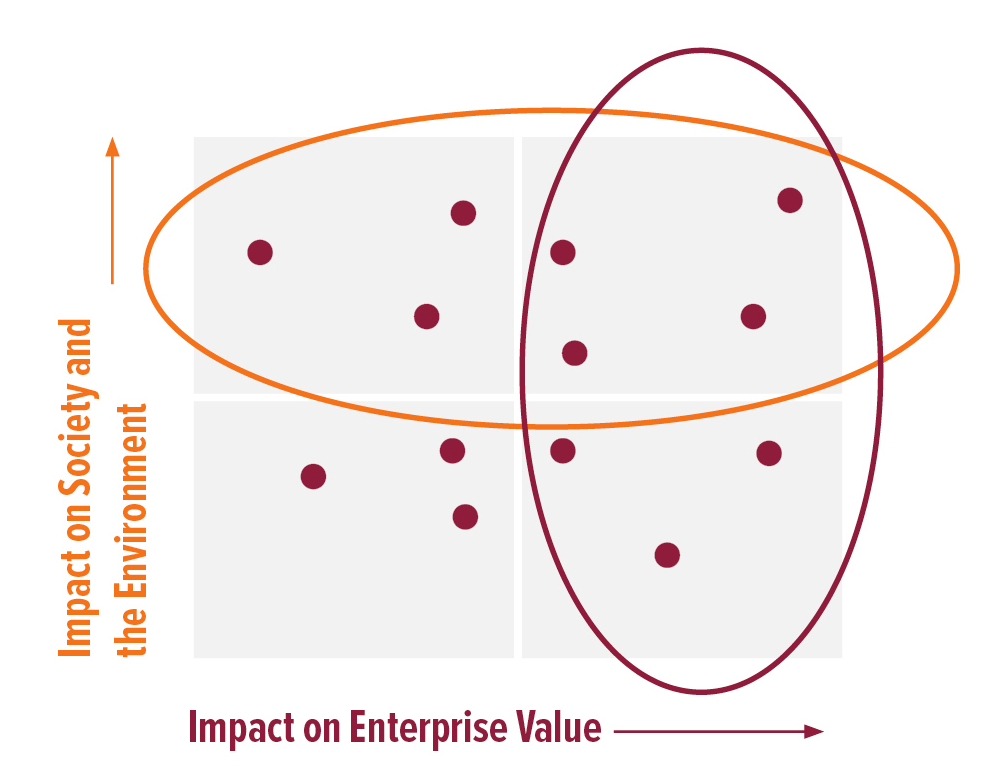

Materiality is a central concept within the debate, especially given the cleavage between Europe and America on the subject. Materiality is the process of identifying which issues are significant for a given issuer or company. As summarized above, if they have a significant effect on the company’s Enterprise Value, issues can be categorized as financially material (right half of the figure below). On the other hand, if they have a significant effect on a company’s stakeholders (clients, suppliers, communities, the planet, etc.), they can be categorized as material for stakeholders (top half of the figure below). Single materiality is taking only the first into consideration. Double materiality takes both into account (top right quadrant).

Figure 3: visualising double materiality

So why is this so important? Well, promoters of single materiality largely argue that Financial Institutions have a fiduciary duty to clients and shareholders and should only consider issues that are financially material. Double materiality promoters largely argue that if we are going to clean up the mess we got ourselves into, well, we need to apply a wider lens. But where it gets interesting is where the former argue that all stakeholder issues are financially material in the long run, and therefore should be taken into account in a single materiality approach. In theory that would be correct. Take for instance the example of an industrial company that unbeknownst to its stakeholders polluted water for neighbouring communities for years. This is bound to become financially material at some point, so should be taken into account in a single materiality analysis.

We argue that in practice this is not the case. A very large portion of financial materiality analysis uses the SASB standards, which currently do not take this long term view. So investors risk missing risks that not only are material from a stakeholder perspective now (which in itself should be an argument for considering them), but will most likely become material from a financial perspective one day or another. That is why we have opted for a double materiality approach in our process.

It is important to note however that while materiality is central, it does not equate to impact management, i.e. an ESG analysis using double materiality does not make it an impact analysis. We would still be missing positive impact analysis (materiality is largely referred to in the context of negative impact analysis), as well as understanding additionality, impact risks, etc. (see impak’s methodology document available on its website for more details).

The impak Score as a measure of impact

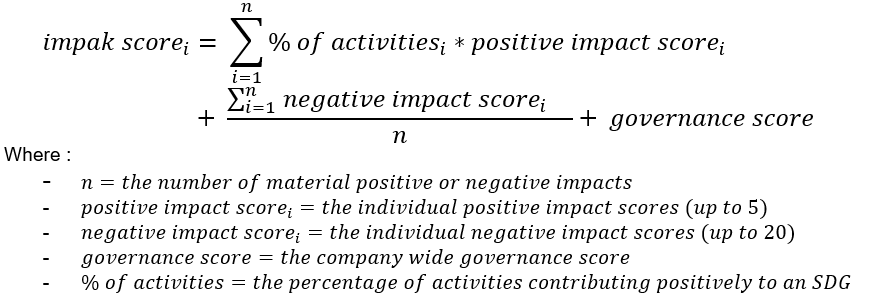

The impak Score was built to rate issuers on their ability to generate positive impacts (linked with SDGs), their ability to mitigate negative impacts, and how they are governed to ensure positive impact generation and negative impact mitigation. It is based on the Impact Management Project Norms and summarizes a multifactor, quantitative and qualitative analysis. With a maximum of 1,000, the impak Score is split in 3 subscores: 500 pts for positive impact generation, 300 pts for negative impact mitigation and 200 points for governance.

In short, positive SDG contributions are validated through a rigorous 5 step approach. Material negative SDG contributions are then identified thanks to our dynamic double materiality analysis fed by a controversy research process.

Next, each IMP criteria gets assigned a weighting, and the algorithm calculates a positive impact score for each (i) positive impact and (ii) identified negative impact mitigation as well as a general, company-wide governance score by summing up the weights associated to each data point in every category. The following formula is finally applied:

One important condition is built into the algorithm in order to respect the Do No Significant Harm principle: if a company has been assigned a Z for one of its negative impacts, its aggregate positive impact score will be discounted, and the associated negative impact score will be brought to 0.

Our impak Score allows Financial Institutions to compare companies together based on a 360° view of a companies’ activities: positive AND negative, Environmental, Social AND Governance impacts, using a double materiality approach. As such, and to replace it in the sustainable investing spectrum in Figure 1, it may be used across the spectrum (except for Philanthropy).

More information on our methodology and the impak Score in our rating methodology document available on our website.

Comparison between impak Scores, SDG Scores and ESG ratings

First things first: all ratings used in this article do not measure the same things. Besides explaining the impak Score above, we summarize hereafter our understanding of what the other ratings measure. It is also helpful to place the various ratings in the graph above to assess what they actually enable investors to do:

- RobecoSAM’s SDG score: measures net contribution to SDGs through products & services sold as well as operations. May be used for Themed investing (not for impact investing for which additional data is required as explained above).

- Sustainalytics ESG rating: measures a company’s exposure to ESG risks using a single materiality approach, and how well it manages those risks, placing issuers in low to severe risk buckets. May be used for Screening or ESG integration strategies.

- MSCI ESG rating: measures a company’s resilience to financially material ESG risks relative to peers (not across industries) using a single materiality approach, and rates issuers as laggards, average or leaders. May be used for Screening or ESG integration strategies.

- S&P ESG rating: measures a company’s ESG risk using a double materiality approach. May be used for Screening or ESG integration strategies, not for themed investing even though it uses a double materiality approach as there is no company positive impact data analysis.

- Refinitiv ESG rating: measures a company’s ESG performance using a single materiality approach. May be used for Screening or ESG integration strategies.

- Impak Score: measures a company’s positive and negative, E, S and G impacts using a double materiality approach. May be used across the sustainable investing spectrum (except for Philanthropy).

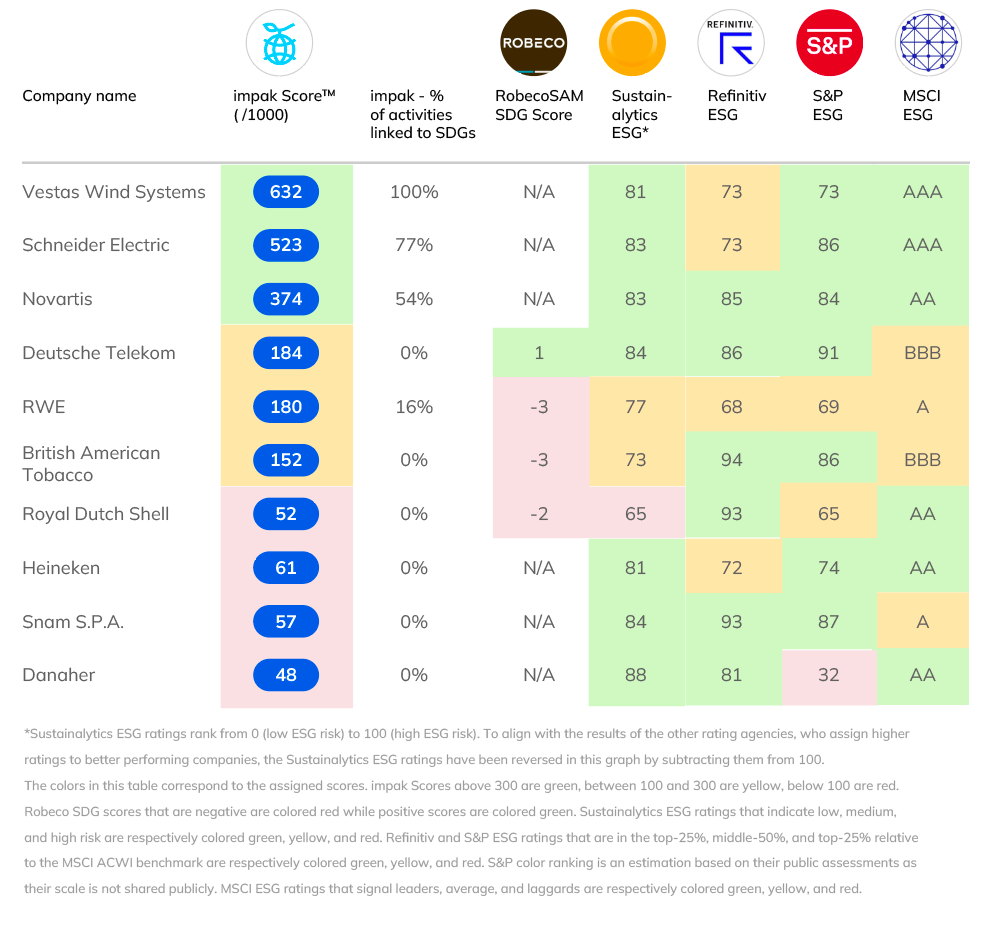

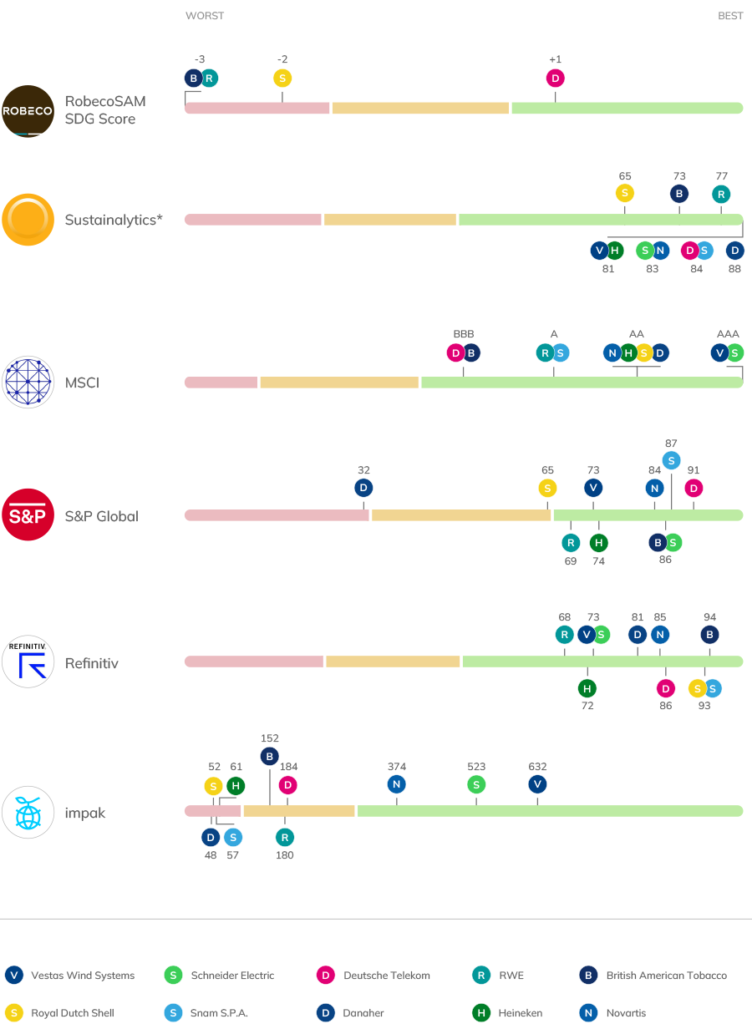

The following table looks at a sample of large international issuers split into 3 groups:

- Impak top 3: the top 3 companies in our universe, also rated by the other providers

- Robeco comparison: 4 companies out of 10 mentioned in the article for which we had an impak Score

- Impak bottom 3: the bottom 3 companies in our universe, also rated by the other providers

Table 1: rating comparison (Part 1)

Table 2: rating comparison (Part 2)

A few anecdotal points are interesting to note when comparing the impak Score to ESG ratings:

- There’s not a whole lot of red on the right hand side of the table, meaning even companies with poor impak Scores (no positive impacts, significant negative impacts and poor negative impact mitigation) get relatively good ESG scores, with 2 exceptions: Danaher for S&P and Shell for Sustainalytics.

- A good impak Score seems to generally translate into a good ESG score as well;

- For some reason, Schneider Electric (a leading energy efficiency company) gets the same rating as British American Tobacco (guess what they do) from S&P, and a better rating from Refinitiv;

- Believe it or not, a leading international oil major can enjoy being attributed high non-financial ratings…at least from some agencies…

Now comparing Robeco’s SDG score to our impak Score:

- Deutsche Telekom, a company with no positive impacts, no links to the SDGs and a Z: May cause harm due to a lack of mitigation activity on its material negative impact on water consumption to generate electricity and cool data centres, gets a Robeco SDG score of +1

- On the other hand, Shell gets a score of -2, whereas RWE, a company with 15% of its revenue linked to SDG 7 thanks to its renewable energy production, gets a -3. We know that RWE has important negative impacts as well (its Scope 1+2 GHG emissions are larger than Shell’s), but shouldn’t they get a slightly better score than a company with no positive SDG contributions?

Going beyond ESG

ESG, by design, is helpless if we are serious about achieving any of our societal goals as materialized in the SDGs. In order to do so, we need contextualised (positive and negative) impact data based on a double materiality approach and covering the entire scope (inter-dependency is at the heart of it here) defined under all of the 17 SDGs. As you can see in the examples above, impact data adds an extra layer of risk management information vs its ESG auntie, and at the same time provides a best-in-class SDG alignment profile. Weeding out the bad apples while also allowing to select the very best thanks to a rigorous, anti-washing methodology. And it gives you credible data to back your (regulation-compliant) claims of saving the world (or not).

Using first generation ESG data today could be compared to investing in the 1920’s (before accounting standards were born) while only looking at a company’s liabilities, not the full balance sheet.

Although this article is largely anecdotal, it will be followed by a deeper analysis. We just couldn’t wait to share some of the insights and to add our views to the debate.

For Financial Institutions out there who want to go beyond ESG and get into the fascinating world of impact, let us know, we’d love to chat. It all starts with impact intelligence.

ABOUT IMPAK FINANCE

impak – the independent impact rating agency – is a Canadian and French start-up that has built impak IS², an impact assessment and scoring solution based on leading international standards, notably the Impact Management Platform and the United Nations 17 Sustainable Development Goals. It has also created a group of impact indices, based on the impak Score™ and other data in the impak database used to develop index funds and ETFs. Through its impact assessment and scoring solution, impak’s primary goal is to channel capital towards businesses with a positive social or environmental impact. impak’s secondary goal is to trigger traditional businesses’ potential of transformation and use the impact assessment as an incentive to truly mitigate their negative impacts and create positive ones. impak contributes to shift the purpose of capital in society while still considering profitability.

DISCLAIMER

No information on this document constitutes a promotion, recommendation, inducement, offer, or solicitation to (i) purchase or sell any securities or assets, (ii) transact any other business, or (iii) enter into any other legal transactions. All information provided in this document is informational, impersonal, and not customized to the specific needs of any entity, person, or group of persons. impak Finance is regulated by the Quebec AMF and complies with EU regulations where applicable. impak’s data and impact assessment methodology are based mainly on the UN’s SDGs and the Impact Management Platform, also including SASB, GRI, etc. impak’s rating methodology is available on its website at https://www.impakanalytics.com/compliance/. This information is subject to impak Finance’s terms of use and compliance policies.

Information used for impak ScoreTM calculations has been collected directly from company disclosures. impak Finance uses the greatest possible care in using information, however it is provided as collected directly from issuers and impak Finance has neither interviewed the issuers’ stakeholders, nor performed an on-site audit nor other test to check the accuracy of the information provided by the issuers. The correctness, comprehensiveness and trustworthiness of the information collected are the issuers’ responsibility.

Sources :

*Corporate Sustainability Performance, Introducing an SDG Score and Testing its Validity relative to ESG ratings, Aug 2022, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4186680

You may also like

2024 ESG Regulatory Landscape

By impak Analytics

Why single materiality is not good risk management

By impak Analytics