impak Battle : EDP vs Engie

About the author: impak, the independent impact rating agency, regularly publishes content providing transparent data on the social and environmental impact of companies. By doing so, it aims to accelerate the transformation towards a stakeholder economy generating an overall positive contribution to society.

About the financial commentator: With nearly €14.7 billion in assets under management, VEGA Investment Managers is the wealth management expertise arm of the BPCE Group – the second largest banking group in France. VEGA IM designs tailor-made financial solutions through its four core businesses: Collective Management, Management Under Mandate, Premium Advisory Management and Fund Selection in open architecture. The company is particularly recognized for its expertise in European markets and its “Growth” management style and has developed a Responsible Investor approach; 10 UCIs in the range are labelled SRI (figures as of 06/30/2022).

The impak Battle - VEGA Responsible Transformation Series

The energy transition of our societies is a subject that can no longer go unnoticed, especially in the current context where Europe feels more than ever its dependence on its foreign gas suppliers. Although the energy sector is still mainly made up of oil and gas companies, some companies have decided to invest in renewable energy. The face to face of this impak Battle is composed of two companies from this sector in change. On one hand, Engie, the largest natural gas distributor in Europe, is a French company active in the distribution of gas and electricity in more than 40 countries. On the other, EDP, a Portuguese electricity supplier operating in more than 19 countries, proudly states that the majority of the energy it produces comes from renewable sources. This impak Battle is based on 2020 data made public by both companies.

🇺🇦 The Ukrainian crisis

Starting in 2022, enterprise responses to the Ukrainian crisis are not part of this analysis. However, as the conflict takes on significant economic and social dimensions in the energy sector, it is important to place Engie and EDP in this situation. Engie affirmed its support for the affected populations and recalled that it had no industrial activity in Russia, although it has a portfolio of contracts from the country in the order of 20% of its international gas sales. As for EDP, which has operations in countries bordering Ukraine, the company has mobilized human and financial resources to work with local agencies and authorities to provide support to the refugee crisis in the region. In particular, the company has offered its support to the Red Cross, Médecins sans Frontières and has created a partnership with the Biedronka Foundation to help Ukrainian refugees in Poland with a donation of €500,000

Positive impacts

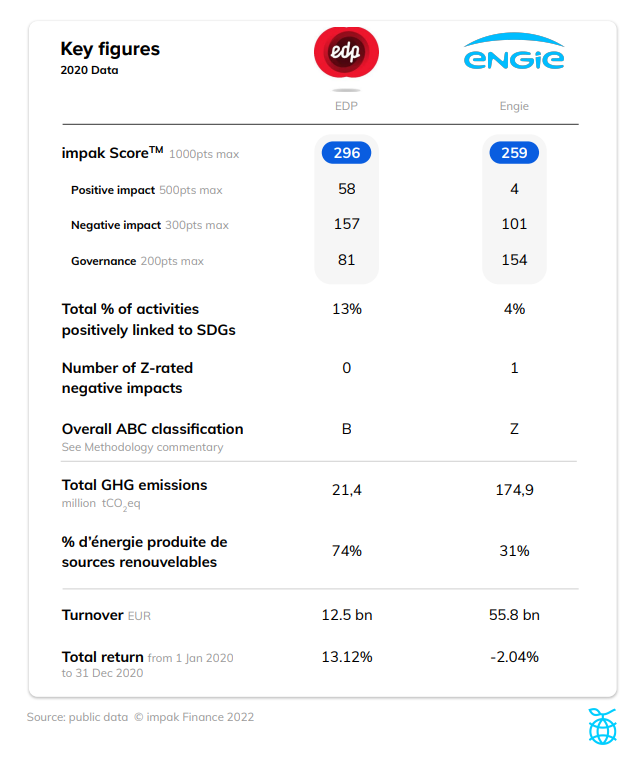

Engie 4/500

Engie’s positive activity is linked to its production of renewable energy. This activity, representing 4% of its turnover, contributes to SDG 7.2 on the share of renewable energy in the global energy mix. However, the company did not score very high due to the small share of its activities and activities rated Z (harm or little harm / see methodological note ). Other positive activities, such as the distribution of energy efficiency tools in Morocco and South Africa were not retained since the information disclosed by the company does not allow to assess the positive contribution of these actions on the beneficiaries. Thus, this positive activity is considered B, which means that it benefits stakeholders (see methodological note).

EDP 58/500 Winner

EDP has two positive material activities representing 13% of the company’s turnover, thus contributing to SDG 7.2 and 7.3 on energy efficiency and the share of renewable energies in the global energy mix. Therefore, EDP devotes 2% of its activities to providing its customers with energy efficiency solutions and products and 11% to the production of renewable energy. The company produces renewable energy through, among other things, hydroelectric power plants, wind farms and solar panels. Both activities are also considered B as they benefit stakeholders.

Why VEGA IM has chosen EDP

VEGA IM has selected EDP, Portugal’s leading electricity producer and distributor, for its 75% renewable energy mix (hydroelectricity, wind, solar) and for its business model's resilience, of which 90% is exposed to regulated activities (electricity generation and networks).

As one of the undisputed leaders in the energy transition space, EDP is continuing its action through a significant investment plan of €24bn over the period 2021-2025 to double its installed capacity in wind and solar and grow its renewable installed base by 20 GW.

In the longer term, its objectives are among the most ambitious in the sector with 100% renewable generation capacity and a carbon-neutral activity by 2030. Moreover, according to VEGA IM, EDP remains a potential target for a player wishing to enter or strengthen itself in the production of renewable energies.

Analysis completed on April 20 2022.

Mitigation of negative impacts

Engie 101/300

Of its 11 material negative activities, only one is rated Z, which means that it harms or can harm the SDG to which it is linked. However, it should be noted that the company has mitigation activities for its other 10 material negative activities, which explains its score of around 100 points. Let’s take a closer look at this Z which is linked to SDG 16 on the protection of fundamental rights and public access to fair information. Engie was involved in two controversies related to false communications, for which the company had to pay fines. The first sum of 1 million euros had to be paid to the Versailles Court because of illicit solicitations with the customers of its competitors. The second fine of 15,000 euros issued by the Paris Court is linked to false commercial offers concerning a reduction in electricity prices during weekends.

EDP 157/300 Winner

On the contrary, none of the 11 negative impacts listed for EDP is rated Z. This means that the company has not been linked to major controversies since 2018 and that it mitigates the entire activities considered material. For a company in the electricity generation sector, the fact that it has no Z and mitigates its 11 negative impacts is noteworthy, due in part to the fact that EDP reports quality indicators for the majority of its negative activities. Finally, because the company has *SBTi-approved GHG emission reduction targets, it is also not Z-rated on climate.

*Science Based Targets initiative, also known as SBT or SBTi - a partnership between the Carbon Disclosure Project (CDP), the Global Pact of the United Nations, the World Resources Institute, and the World Wildlife Fund

Governance

EDP 81/200 Engie 154/200 Winner

This sub-score is by far the highest for Engie. The company is supported by a governance structure that not only integrates a mission of impact within the company but analyzes a large part of its value chain on environmental and social impact issues. Although both companies have shortcomings related to the participation of beneficiaries in decision-making, Engie has a more developed communication system, better integrating them into the company’s decision-making process.

EDP wins 🎉

With a final score of 259 for Engie and 296 for EDP, the battle between these two companies in the energy sector proved to be a tight one. However, EDP prevailed thanks to the positive impacts it generates (14% of its operations) and the mitigation of all its physical activities. As for Engie, it is penalized by its communication controversies and the small share of its activities linked to a positive impact.

Climate goals

It is no secret that businesses play a central role in the fight against climate change, especially in the energy sector. But not all take on this role with the same importance. Indeed, Engie has a plan to reduce its GHG emissions in line with the 2-degree trajectory recommended by the Paris climate agreement. While this goal may seem acceptable, it is far less ambitious than that of its peers in the sector. EDP, for its part, has integrated a plan to reduce GHGs in line with the 1.5 degree trajectory; a more ambitious trajectory and in line with the climate challenge.

Methodological Notes

The methodology follows the IMP classification: A (Acts to avoid Harm), B (Benefits stakeholders), C (Contributes to solutions), and Z (Does or may cause harm). Note that according to our methodology, in the case of a Z, a certain penalty is assigned based on the following 3 factors: the type of Z (does cause harm or may cause harm), the repetition of the Z over time and, only in the case of a Z that ”does cause harm”, whether measures have been taken to mitigate this negative impact.

It is important to mention that companies may have some potential positive impacts that were not considered because of the limited information available or because they represent less than 0.01% of their activities. As positive impacts are based on their relationship to the Sustainable Development Goals (SDGs), they can overlap. The percentages of activities related to these impacts can therefore be non-cumulative.

The sub-score related to governance is based on several criteria analysing the integration of impact mechanisms within the company. Thus, the role of the various beneficiaries in decision-making, the analysis of its impacts within the value chain and the assignment of a team dedicated to the impact mission are all important criteria for this section.

Given the significant growth in transparency and sustainability among investors, one or two years can make a significant difference to impak Scores.

*VEGA Investment Managers is in no way responsible for the information contained in this article. The analysis of VEGA IM does not constitute investment advice or recommendation.

VEGA INVESTMENT MANAGERS - 115, rue Montmartre, CS 21818 75080 Paris Cedex 02

Tél. : +33 (0) 1 58 19 61 00 - Fax : +33 (0) 1 58 19 61 99 - www.vega-im.com

A public limited company with a board of directors having a capital of 1 957 688,25 euros - 353 690 514 RCS Paris- TVA : FR 00 353 690 514

Asset management company, approved by the Autorité des Marchés Financiers (AMF) under the number GP 04000045 - headquarter : 115, rue Montmartre 75002 PARIS

IMPAK RATINGS INC - 5605, avenue de Gaspé, Montréal, QC H2T 2A4

Did you find this impak Battle insightful?

Leave us your email below to receive our latest publications.

You may also like

impak Battle : Air Bus vs Alstom

By impak Analytics

Why single materiality is not good risk management

By impak Analytics