impak Battle : Air Bus vs Alstom

The Supply Chain

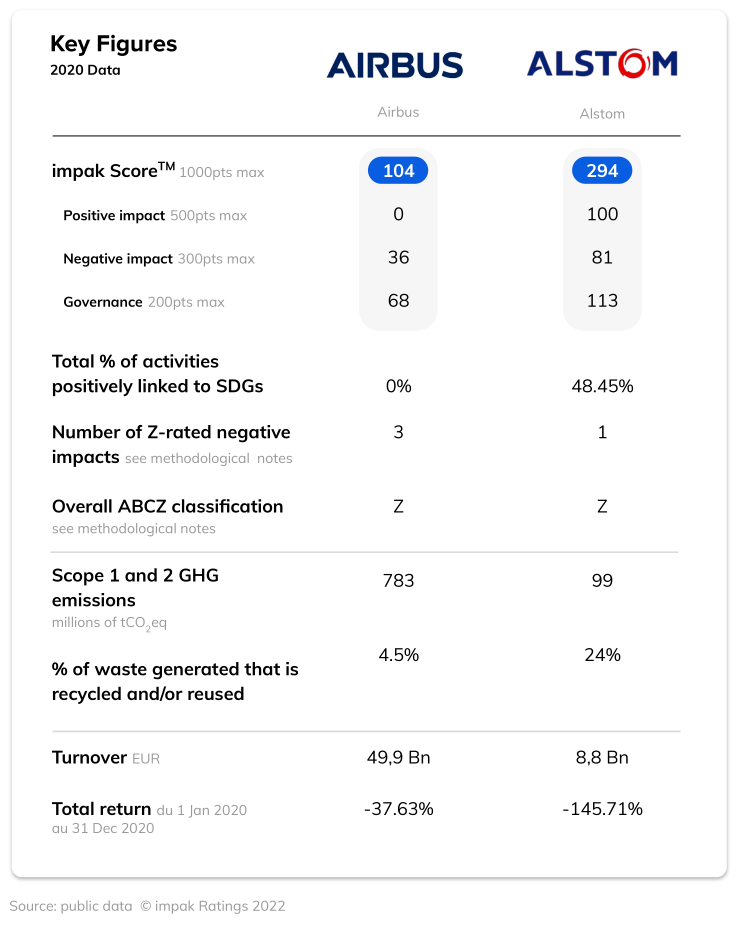

A company's supply chain is the network of actors that contribute to the production of a good, from the mining companies to those that sell the product to the consumer. This supply chain is important in any analysis of the environmental and social impacts of companies. In particular, it allows us to complete an impact study with those activities that are unknown and invisible to the end consumers. This case study focuses on companies that manufacture airplanes and trains, thus taking a deep dive into the supply chain of the transportation industry. In this impak battle, we went further into the sub-tiers of the transportation industry’s supply chain, touching upon the suppliers of these manufacturers with the Alstom controversy.

You may also like

impak Battle : Michelin vs Renault

About the author: impak, the independent impact rating agency, regularly publishes content providing transparent data on the social and environmental impact of companies. By doing...

Are companies prepared for CSRD?

Are companies prepared for CSRD? And what that means for Financial Institutions. CSRD can be a massive market opportunity or your biggest headache depending on...

Why agribusiness giants won’t save the world from hunger.

Why agribusiness giants won’t save the world from hunger. A study of the contribution of the agrobusiness to SDG 2 Download Study Against a backdrop...