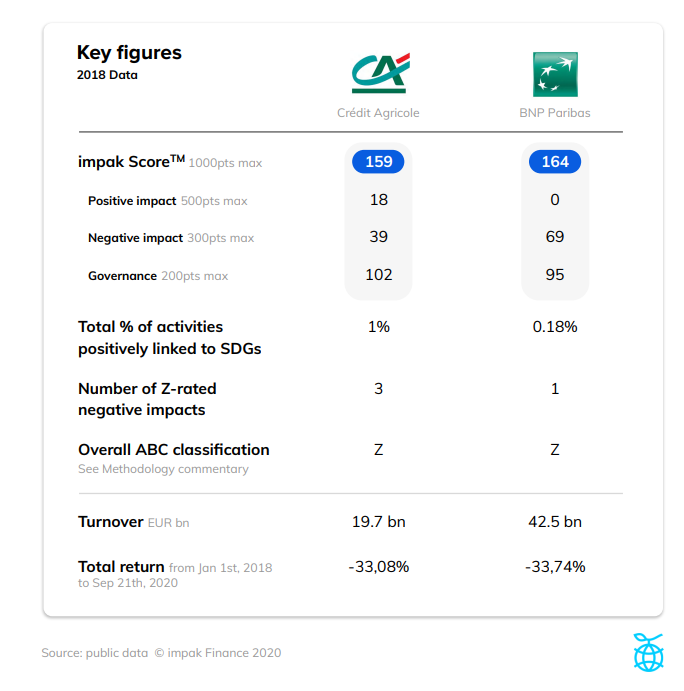

impak Battle : Crédit Agricole vs BNP

Specificity of the sector

The current critical social and environmental events happening worldwide bring a new stance on the importance of banking. Climate change, which exacerbates social inequalities, is simultaneously the biggest negative impact for banks, but also an opportunity to do good on a massive scale. The sanitary crisis has enhanced this opportunity as banks are key actors in the different countries’ recovery plans, in which some countries have been bold enough to attach climate and social targets. The sector’s biggest liability could become its strongest asset if rightfully managed and in a timely fashion. Banks brought the Western world as we know it to life, we shall hope this blatant wake-up call will turn them into agents of impact.

You may also like

impak Battle : Air Bus vs Alstom

About the author: impak, the independent impact rating agency, regularly publishes content providing transparent data on the social and environmental impact of companies. By doing...

Why single materiality is not good risk management

Why single materiality is not good risk management Recent news about the Moody’s ESG – MSCI partnership has stirred up an old debate about the...

Why agribusiness giants won’t save the world from hunger.

Why agribusiness giants won’t save the world from hunger. A study of the contribution of the agrobusiness to SDG 2 Download Study Against a backdrop...