Impact portfolios outperform both S&P 500’s and MSCI World’s

Impact portfolios outperform both S&P 500’s and MSCI World’s

A disruptive launch

We were very proud to announce the launch of the five first true impact indices and ETFs on the London Stock Exchange, on June 7th, 2023 with our client Circa5000 and partner Bita. A truly historic moment for impact investing!

The question we got asked almost instantly was: “How are they performing?” “Very well, thanks!”, we answered. “Oh you mean from a financial perspective? As it turns out – overall, pretty good as well”.

In this short case study, we look at an equally weighted sample impact portfolio of 62 impact stocks (top impact performers, all rated Bs or Cs as per the Impact Management Project (IMP) methodology and with significant UN SDG contributions) and compare it to market indices.

We start with a quick refresher on impact theory, how we constructed the impact indices and the sample impact portfolio, then dive into the impact and financial analysis.

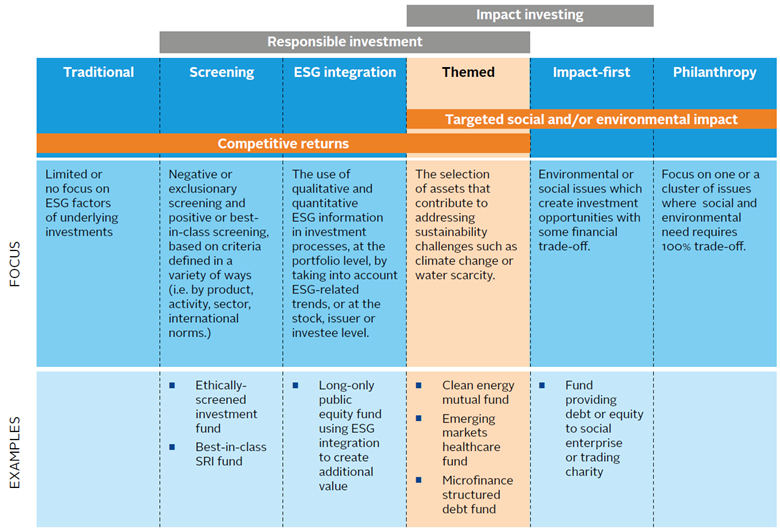

ESG vs Impact 101

Sustainable financing or investing has become a very broad term that encompasses many things. We like to use the following to visualize the spectrum of options available to lenders and investors.

Figure 1: the sustainable investing spectrum

Source: UN Principles for Responsible Investment (PRI)

Now, a few consensual definitions around impact:

- An impact is a change in an outcome caused by an organization. An impact can be positive or negative, intended or unintended.

- An outcome is the level of well-being experienced by a group of people, or the condition of the natural environment, as a result of an event or action.

- Impact management is the process of identifying the positive and negative impacts that an enterprise has on people and the planet, and then work to reduce the negative and increase the positive.

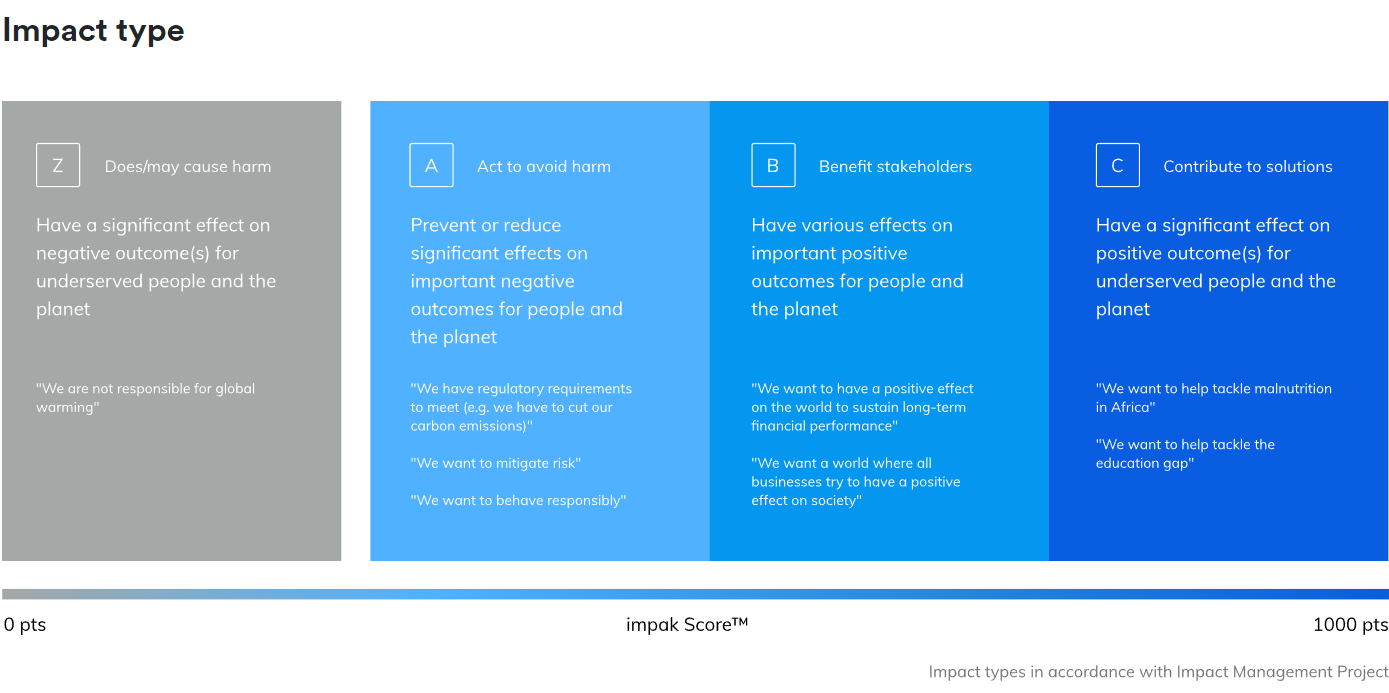

Another useful way to look at it is by using the ABCs of impact management developed by the Impact Management Project (now housed at Impact Frontiers), with which the impak methodology and impak scoreTM is aligned. So high ESG-scoring companies would be in the A category, and low ESG-scoring companies would be in the Z category. But ESG does not capture the Bs and the Cs.

Figure 2: the ABCs of impact management

About our indices

Circa5000, a BCorp and disruptive UK-based impact investing company, was looking for a data provider in order to offer cost-effective impact investing strategies. Our client was looking for a partner (i) able to offer customized impact-enhanced ESG indices to create their own ETFs and (ii) provide the most granular, reliable and rigorous data in order to identify real positive impact contributions.

“We couldn’t find impact ETFs that had an impact-focused selection and weighting methodology, so we decided to create our own. Impak is the only data provider whose methodology is based on the rigorous IMP Norms and therefore going beyond ESG and SDG alignment. The 30-page impak reports provide a robust and transparent rationale behind every company we invest in making our products in keeping with the best impact funds in the world”.

– Charlie Macpherson, Head of Investments at Circa5000.

Circa5000 defined the themes above, and with our partner Bita as index administrator and calculation agent we set out to meet this challenge. Starting from the Bita Global Impact Universe, composed of global, publicly-listed securities whose products and services were mapped to the themes, impak applied an additional impact screening and rated and scored the filtered universe. Securities were then ranked by impak Score and the top 75 were selected as constituents. If there were fewer than 75 eligible securities, all securities were selected as constituents. This was a challenge in itself as there is a clear lack of impact-driven listed companies on stock markets (if even Patagonia calls itself an unsustainable company, the bar is and should be high).

Impact companies vs. the broader market

Below we present the findings of our research on the sample impact portfolio that we have constructed, which combines five eligible impact universes: Health & Wellbeing, Social & Economic Development, Green Energy & Technology, Clean Water & Waste, and Sustainable Food & Biodiversity. Our objective was to identify and create an equally-weighted portfolio consisting of the most impactful performers within these universes. We selected companies that not only generate positive impacts B: Benefits Stakeholders (for example through selling products that support good health or educational outcomes) but also C: Contributes to Solutions that address pressing social and environmental challenges (such as enabling an otherwise underserved population to achieve good health or educational outcomes, for example).

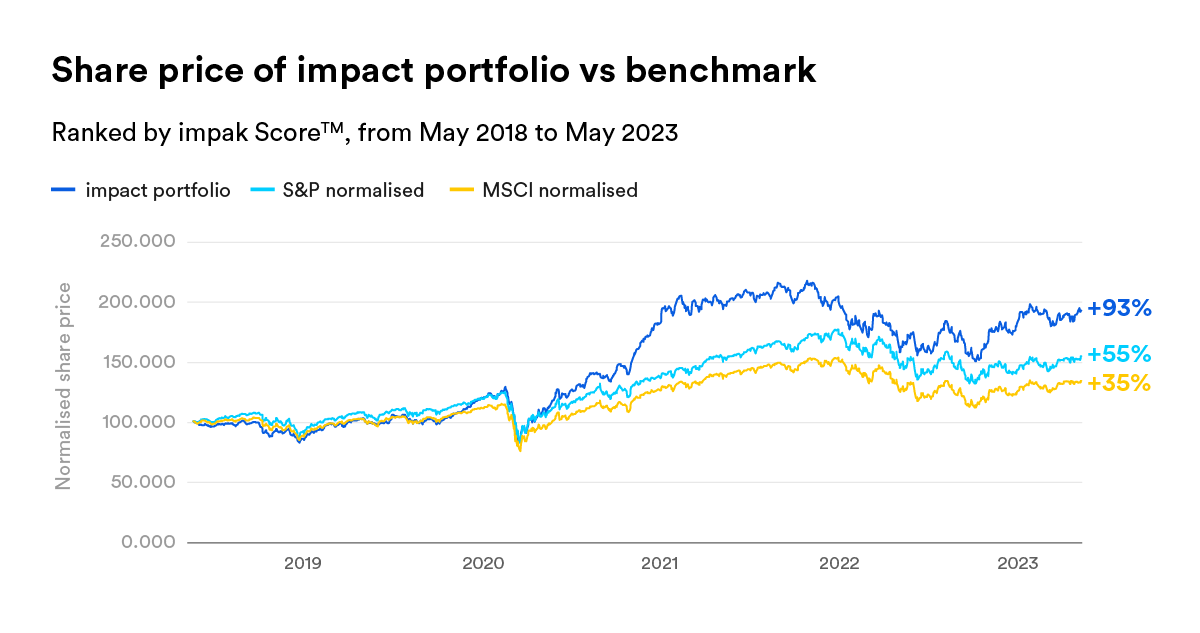

The constructed portfolio has demonstrated strong outperformance in the post-COVID period. The green economy played a pivotal role, with stocks in solar power, semiconductors, and transitioning industries delivering robust returns. While recession concerns caused a temporary setback in the second half of 2021, the portfolio has since rebounded and outperformed as markets stabilized (see the chart below). This resilience speaks to the growing importance and financial sustainability of the green economy. All in all, investing in the basket of our most impactful companies five years ago would have yielded a total return (excluding dividends) of 93%, outperforming the S&P 500’s return of 55% and the MSCI World’s return of 35%.

Figure 1: Share price of impact portfolio vs benchmark

The chart above represents the performance comparison of the equal weight basket of Circa5000 impact stocks against the S&P 500 and MSCI World indices over a five-year period. The initial value of the basket, along with the S&P 500 and MSCI World indices, was set to 100, allowing for a like-for-like comparison.

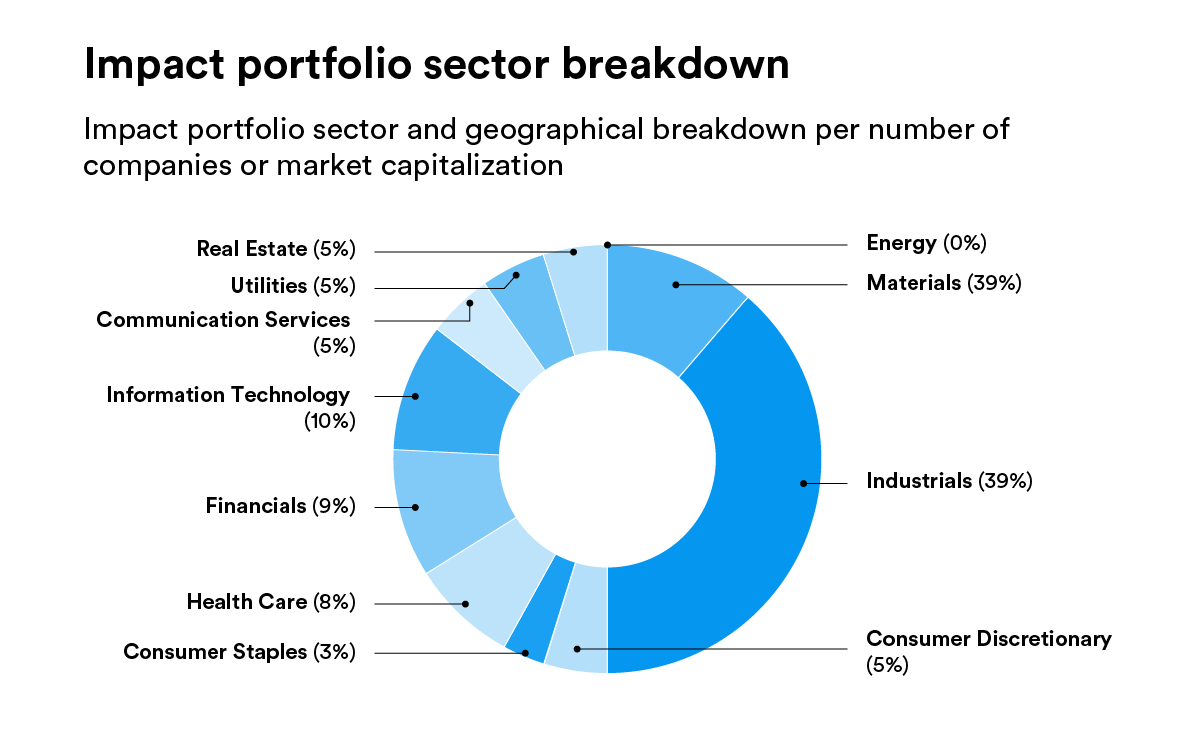

Figure 2: impact portfolio sector breakdown

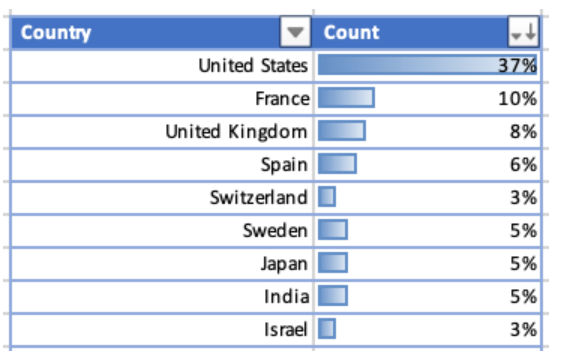

The chart and table above show the impact portfolio sector and geographical breakdown per number of companies or market capitalization. Source: impak, Factset.

Figure 3: impact portfolio geographical breakdown

The portfolio’s outperformance seems to be driven by the green energy stocks (mainly renewable energy production and energy efficiency, see our Vestas case) and the acceleration of sustainable practices, which exemplifies the long-term viability of sustainable investing. With sustainability now a mainstream trend, the green energy sector is poised to maintain its position as a driving force. Meeting the global energy sector’s ambitious goal of achieving 60% clean energy production by 2050 requires a substantial investment estimated at $100 trillion (as indicated by the International Renewable Energy Agency). Lower production costs, growing climate change concerns, evolving energy policies, and investor pressure around ESG policies will continue to accelerate the adoption of renewable energy.

However, not all green energy companies are created equal. The Do No Significant Harm (DNSH) concept is of paramount importance in this and other sectors, as companies that do not mitigate their negative impacts are exposed to short-term risk of controversies (see Teleperformance’s case), ESG risks and long term revenue exposure risk. The first step in making an investment decision about a prospective stock is therefore to have a 360-degree view of its positive SDG alignment and ESG risks.

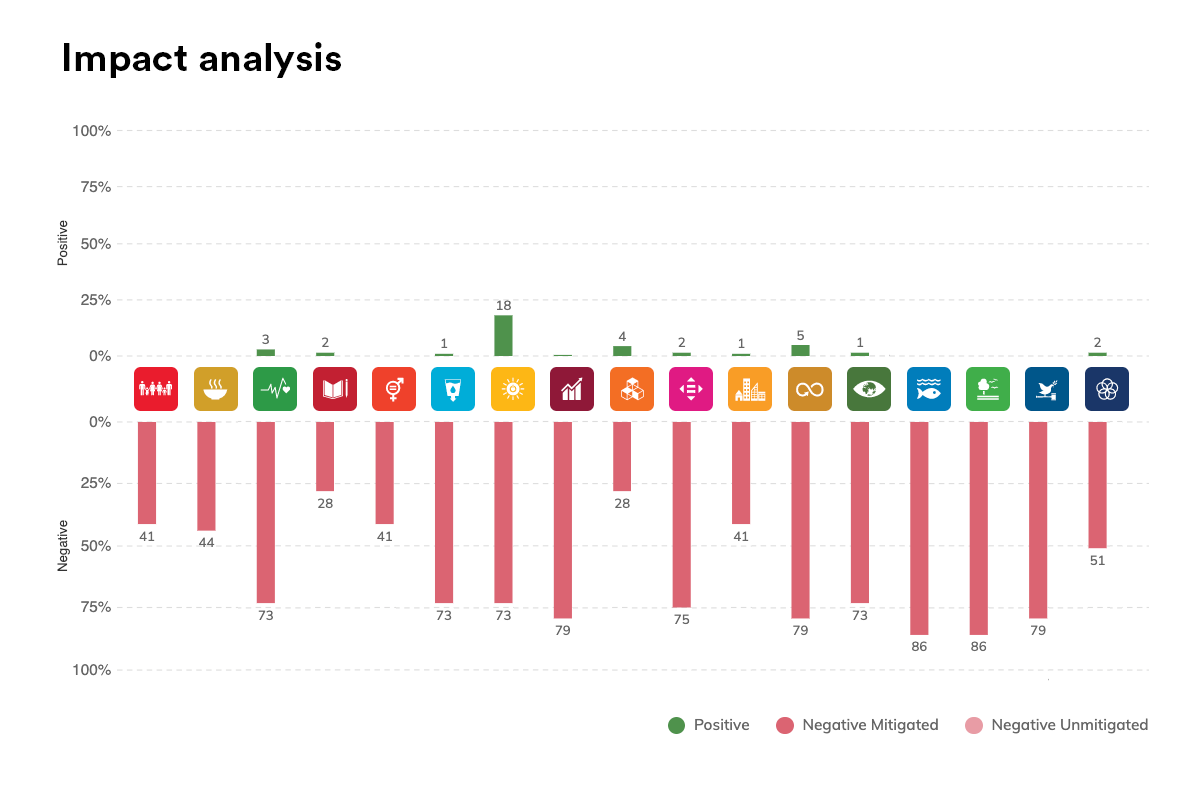

Impact analysis

Here is the aggregated SDG alignment for the impact portfolio. To note that the impact portfolio is positively aligned with a high number of SDGs.

Figure 4: SDG alignment for the impact portfolio

The impact portfolio aggregated SDG alignment

The possibilities for positive impact are infinite as there could be as many as the number of existing companies. On the other hand, companies share more or less the same types of material negative impacts. Why? All businesses, whatever their purpose, require energy and water, depend on natural resources, recruit staff, and have some form of physical presence (e.g. buildings, fields, roads).

As such, we expect companies to at least attempt to avoid or reduce their harmful impact. Companies that do not mitigate their negative impact completely may jeopardize their licence to operate or face increased reputational risk, but we’ve made sure to exclude such companies from the impact portfolio, which ensures that the portfolio properly mitigates all its negative impact.

Moreover, not only do the selected companies implement measures to minimize their negative impact but they also prioritize actions that generate the greatest positive impact possible through their own business models. In this way, they focus on optimizing the value generated for the environment and, more particularly, for vulnerable stakeholders.

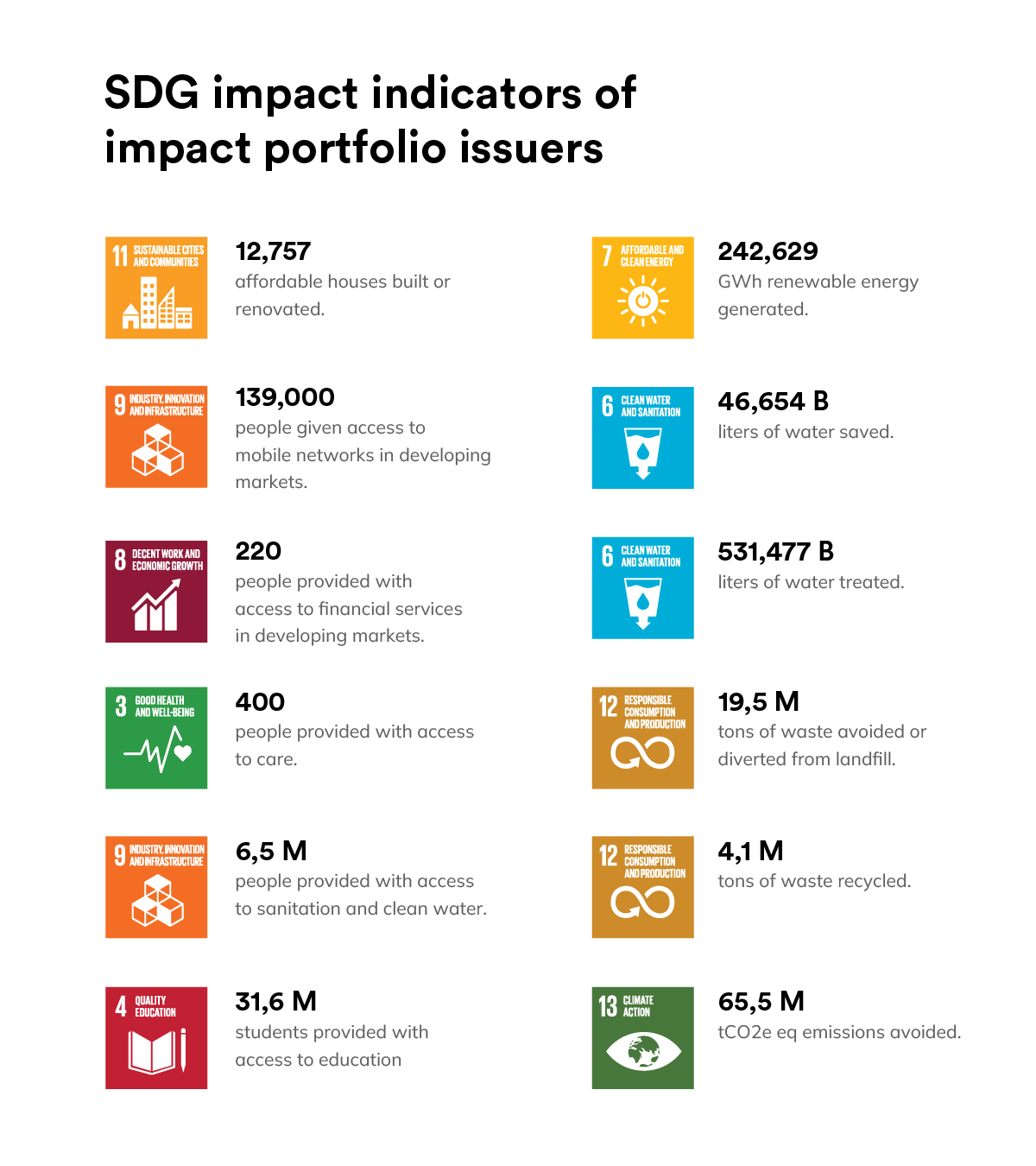

Finally, here are some examples of what the portfolio achieved in terms of output and outcome indicators:

Figure 5: SDG impact indicators of impact portfolio issuers

Conclusion

In light of the current climate crisis, the importance of investing in organizations based on their true social and environmental impact is obvious. To direct the trillions of dollars needed to make significant progress towards the SDGs the finance sector needs to be perhaps more convinced that investing in better companies leads to better performance.

This article (and the ETFs, indices and impact portfolio upon which it is based) adds to our now growing body of research showing that companies creating positive impacts, addressing SDGs and including stakeholders in their decision-making have and will add more value to consumers and investors in the long term, and will steer the global economy towards a greener and more sustainable one. To act on this argument, money managers and issuers need to rely on international frameworks and standards, and data that are transparent and accurate enough to enable comparison and a true economic paradigm shift. CIRCA5000 has therefore decided to publish the full impact reports of the fund’s constituents.

It has been shown that, by investing in impactful companies that address social and environmental challenges, investors can achieve both financial returns and contribute to positive global change. We firmly believe that sustainability will continue to drive investment decisions, making our portfolio an attractive choice for investors seeking to align their financial goals with their values and with the SDGs.

ABOUT IMPAK RATINGS

impak – the independent impact rating agency – is a Canadian and French start-up that has built impak IS², an impact assessment and scoring solution based on leading international standards, notably the Impact Management Platform and the United Nations 17 Sustainable Development Goals. It has also created a group of impact indices, based on the impak Score™ and other data in the impak database used to develop index funds and ETFs. Through its impact assessment and scoring solution, impak’s primary goal is to channel capital towards businesses with a positive social or environmental impact. impak’s secondary goal is to trigger traditional businesses’ potential of transformation and use the impact assessment as an incentive to truly mitigate their negative impacts and create positive ones. impak contributes to shift the purpose of capital in society while still considering profitability.

DISCLAIMER

No information on this document constitutes a promotion, recommendation, inducement, offer, or solicitation to (i) purchase or sell any securities or assets, (ii) transact any other business, or (iii) enter into any other legal transactions. All information provided in this document is informational, impersonal, and not customized to the specific needs of any entity, person, or group of persons. impak Finance is regulated by the Quebec AMF and complies with EU regulations where applicable. impak’s data and impact assessment methodology are based mainly on the UN’s SDGs and the Impact Management Platform, also including SASB, GRI, etc. impak’s rating methodology is available on its website at https://www.impakfinance.com/compliance/. This information is subject to impak Finance’s terms of use and compliance policies.

Information used for impak ScoreTM calculations has been collected directly from company disclosures. impak Finance uses the greatest possible care in using information, however it is provided as collected directly from issuers and impak Finance has neither interviewed the issuers’ stakeholders, nor performed an on-site audit nor other test to check the accuracy of the information provided by the issuers. The correctness, comprehensiveness and trustworthiness of the information collected are the issuers’ responsibility.

You may also like

Annual impak Score review

By impak Analytics

Are companies prepared for CSRD?

By impak Analytics