An early look at how companies with positive contributions to SDGs perform in a financial downturn

2019 was the year of stakeholder capitalism. 2020 might be the year of its demise, or at least the year it will be put to the test. In a period of financial stress due to the recent coronavirus outbreak, will companies keep their climate commitments, will the support of longer-term ESG and impact investors be enough to overshadow the voices of short-termism?

As the Financial Times put it, we believe “what companies should do is clear. What they choose to do will determine which ones emerge strongest.”1

Since its rise in popularity after the 2008 crisis, ESG analysis and the data underlying it have never really endured a recession. We thought it might be interesting to take a closer look at how the best-rated companies in France, one of the markets hit hard by the outbreak, fare compared to their peers.

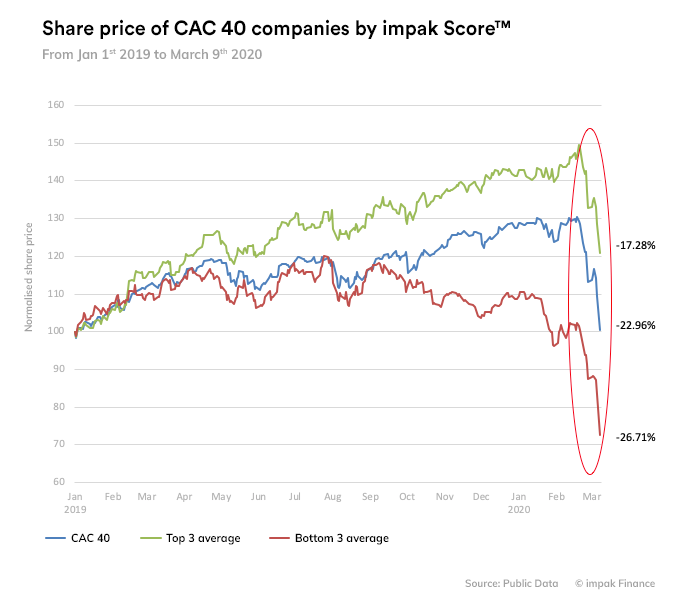

Of course no conclusions can be drawn from such an analysis stemming from a small sample2 but it is interesting to see that the average share price of the top 3 impak ScoresTM in the CAC 40 lost 17.28% during the period Feb 19th to March 9th, 2020, whereas the CAC 40 lost 22.96% and the average bottom 3 fell by 26.71%.

Impact Alpha

This could be an early indication of the existence of impact alpha, i.e. that companies who really integrate the SDGs in their strategy could not only over perform in a bull market but also be more resilient in a bear market. And could be an additional argument for adding a new bottom line to our outdated accounting system.

The top 3 companies are Schneider Electric, Legrand and Danone; the bottom 3 are TechnipFMC, Total and Pernod Ricard. The top 3 were selected because of the significant drop in impak ScoreTM between #3 and #4. It is important to note that there might be a sector bias in this analysis, however the main reason for the difference in impak ScoreTM – as described in our Rating Methodology – is not the sector, rather (i) business model links with SDGs and (ii) the company’s negative impact mitigation performance (whether the company is an A – act to avoid harm or a Z – does or may cause harm as per the IMP framework).

1 Andre Edgecliffe-Johnson, 2020. “Coronavirus poses big test of capitalism’s stakeholder conversion”, Financial Times, March 4, 2020, https://on.ft.com/39DY099.

2 See the full CAC 40 ranking and our Rating Methodology compliant with the Impact Management Project framework and with the UN’s Sustainable Development Goals.

You may also like

2024 ESG Regulatory Landscape

Why single materiality is not good risk management